Business Interruption Insurance: Possible Recovery Option for Small Businesses?

We have had dozens of conversations over the past serval days with both small business owners and landlords and one specific topic seems to be on everyones mind of late: Business Interruption Insurance (“BII”). Quick primer from wikipedia if you are unfamiliar here.

Certain BII intricacies were first put on my radar Saturday by Chef Michael Scelfo of Alden & Harlow, Waypoint and Longfellow in Cambridge (FYI he’s a must follow on instagram right now for his ongoing advocacy for restaurants: @mscelfo). Through the weekend there was a small group of us in constant contact on this issue, including a few public officials, business district leaders, and chefs/owners, all of us scrambling to understand if mandated closures by municipalities would help support a claimant under a BII policy.

Today, sadly, I continue to believe the answer to this question (will BII be a recovery option for tenants?) is no.

My understanding of this matter has been aided by some of my lawyer pals, input from a few insurance agents working for friends and family, and a wildly clear and valuable call I had yesterday with Abby Krueger at Licata Risk Advisors here in Boston. Cliff notes from my research to date:

- The trigger for BII is “direct damage to property.” Lacking physical damage on premies (or nearby) will preclude most claims. It’s the nearby physical damage argument that allowed restaurants and retailers in Back Bay to recover post the Boston Marathon Bombing (this is the example everyone in Boston seems to be referencing of late). Further, in the case of the Boston Marathon Bombing, insurances companies weren’t going to deny a small number of claimants even if the claims weren’t rock solid based on the optics of the situation alone. Unlike the Marathon example, the claimant class for COVID-19 is so massive here that optics are likely irrelevant.

- Some of the restaurateurs and LLs I’ve spoke to in the last 24 hours have flagged a section of most BII polices that details “losses from closures due to civil authority” (or something like this)… but the underlying trigger still needs to be direct physical damage or other actual casualty within a specific distance of the premises, commonly within one mile.

- There are a very small group of food service businesses that may have a rider for “communicable diseases” or “pandemics” but it’s unlikely. My understanding though is that even if this is the case, how do you prove the premises and operations were closed due to direct damages from COVID-19? The fact pattern we are dealing with today is dissimilar from a closure by a city due to something like salmonella or e.coli that derives from a specific business or supply chain.

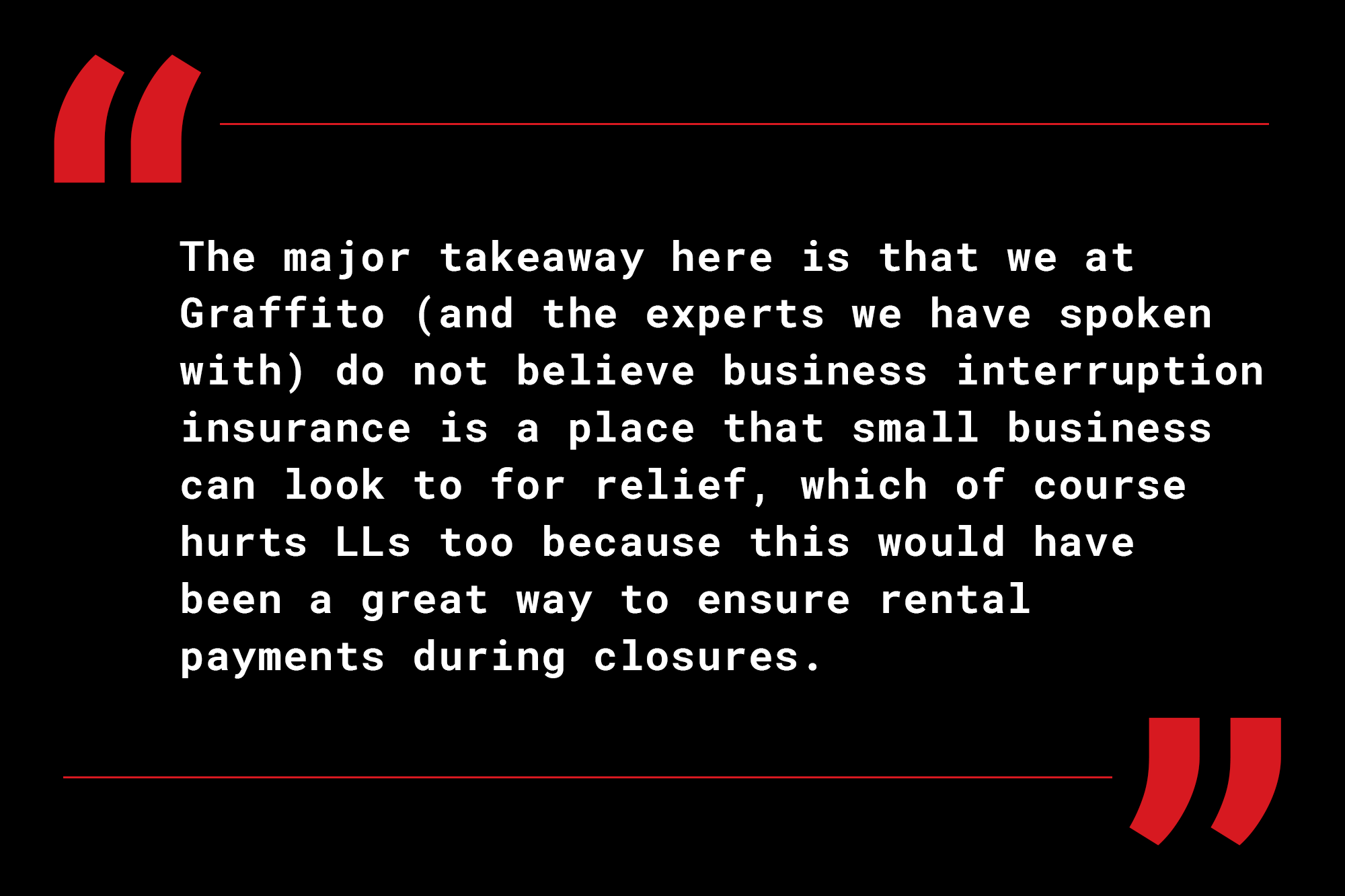

I know this is a bit in the weeds, but the major takeaway here is that we at Graffito (and the experts we have spoke with) do not believe business interruption insurance is a place that small business can look to for relief, which of course hurts LLs too because this would have been a great way to ensure rental payments during closures.

A few last pieces to put on your radar given very recents news:

- The first case in the country on this specific issue was filed yesterday in Louisiana. It is dubious reasoning given what we’ve heard, but worth tracking. Link here.

- NJ lawmakers are discussing legislation to require insurance providers extend coverage to certain small businesses that have BII, in effect shifting the burden to private insurance companies instead of state and federal governments. This also seems unlikely to work, will drive up insurances prices moving forward, and is, frankly, complicated. The best overview I found on this in my quick online search is this article: https://www.jdsupra.com/legalnews/new-jersey-legislature-considering-bill-23908/

I hope we are wrong here, please do not take the above as legal advice (it’s not), and please please let us know if you are hearing anything to the contrary.

We’ll continue to track this.

- Abby Krueger

- Alden & Harlow

- Business Interruption Insurance

- COVID-19

- Insurance

- Licata Risk Advisors

- Longfellow

- Michael Scelfo

- Waypoint