Business Interruption Insurance: Part 3 (From the Experts)

As I noted in my last post on business interruption insurance, the political and legal landscape is rapidly evolving on this matter. We remain in touch with both legal and insurance experts and the most recent communication to share here is from Attorney Eric Allon of Bernkopk Goodman LLP. In addition to being a friend, Eric is top of my list when I have a complicated real estate issue to flesh out. Eric has done work for restaurants and also some of the regions most active landlords. Currently we are working with him on Clover leases (he reps Clover) and also on Market Central leasing (he reps our LL client). His advice below is right on and goes one step further than what Abby recommended last week: Business should not only prepare to file a claim, but they should in fact go ahead and file a claim now.

***

Hi Jesse-

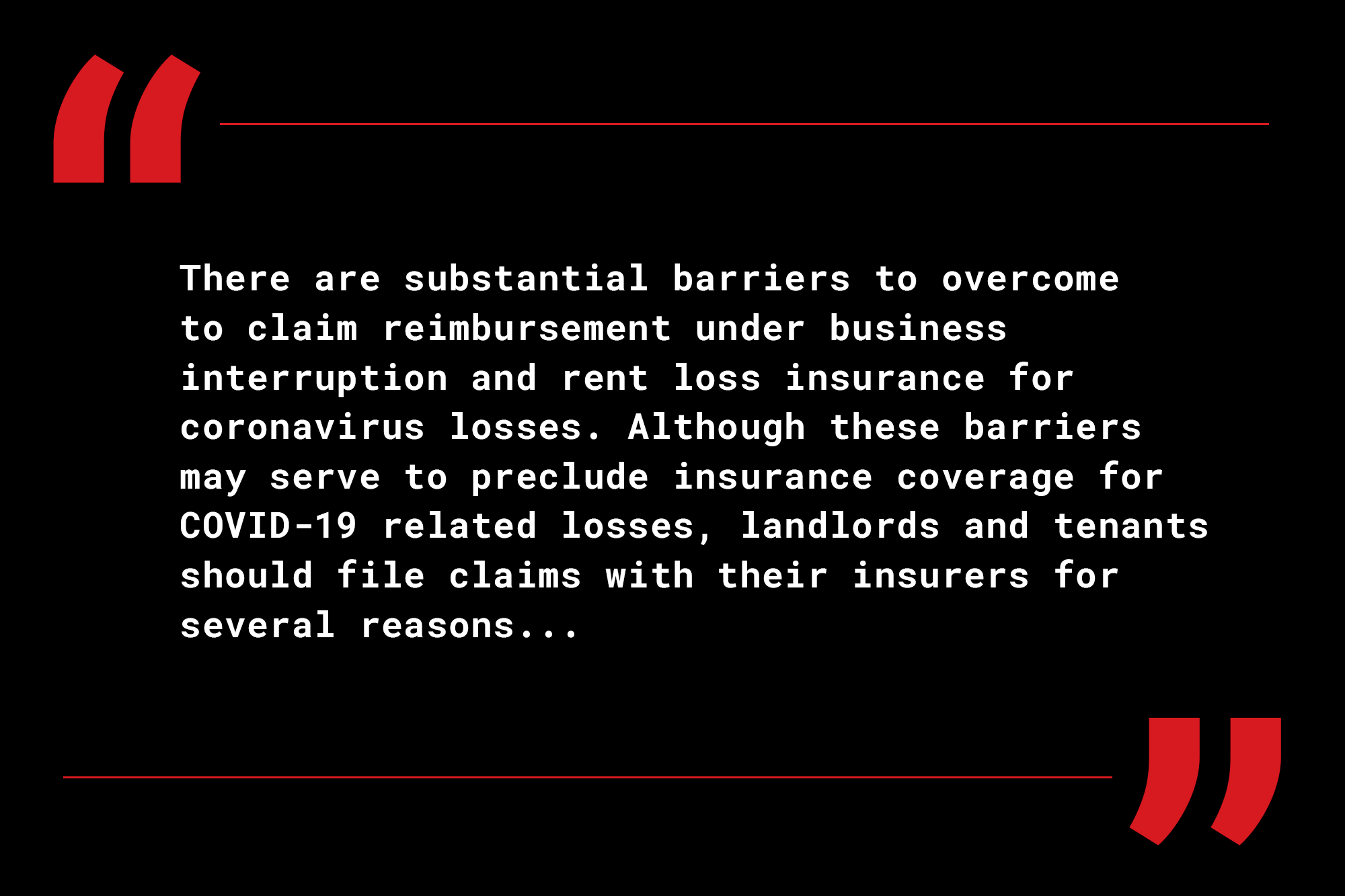

There are substantial barriers to overcome to claim reimbursement under business interruption and rent loss insurance for coronavirus losses. Although these barriers may serve to preclude insurance coverage for COVID-19 related losses, landlords and tenants should file claims with their insurers for several reasons:

- the insurance company has the burden to prove that there is no coverage under the policy and are obligated to investigate all relevant facts and circumstances surrounding a claim and evaluate coverage under the policy.

- There may be governmental intervention or court decisions that could compel insurers to pay losses. There are ongoing legislative discussions in multiple states on this topic. New Jersey legislators are already looking into insurance coverage matters related to COVID-19. A restaurant in New Orleans has already filed suit seeking coverage. I anticipate class actions suits to follow.

- The state or federal government may offer a subsidy program at some point that would reimburse companies for additional expenses and lost revenues due to COVID-19. It is important to keep detailed records to support a claim. Also, any governmental assistance program possibly may require evidence that an insurance claim has been submitted and denied.

In any event, in addition to documenting COVID-19 related losses, please keep records of any governmental actions that require your closure or eliminate or limit access to your building(s), any notices regarding COVID-19 cases in your building or other evidence related to business losses that you suffer or will suffer as a result of COVID-19.

Please feel free to share with your clients and call me with any questions.

Best

Eric

Eric R. Allon, Esquire

Bernkopf Goodman LLP